Quarterly Investment Update - July 2025

Welcome to our quarterly market update. In this month’s market commentary, we are looking at the prior quarter and covering the topic of investing in bonds in a higher interest rate environment. If you have any questions or would like to talk about this more deeply, please reach out to your advisor.

Market Commentary: What Mattered Last Quarter

Volatility in the second quarter and ultimate recovery reminds us why staying invested through uncertainty allows portfolios to capture growth while aligning with long-term goals.

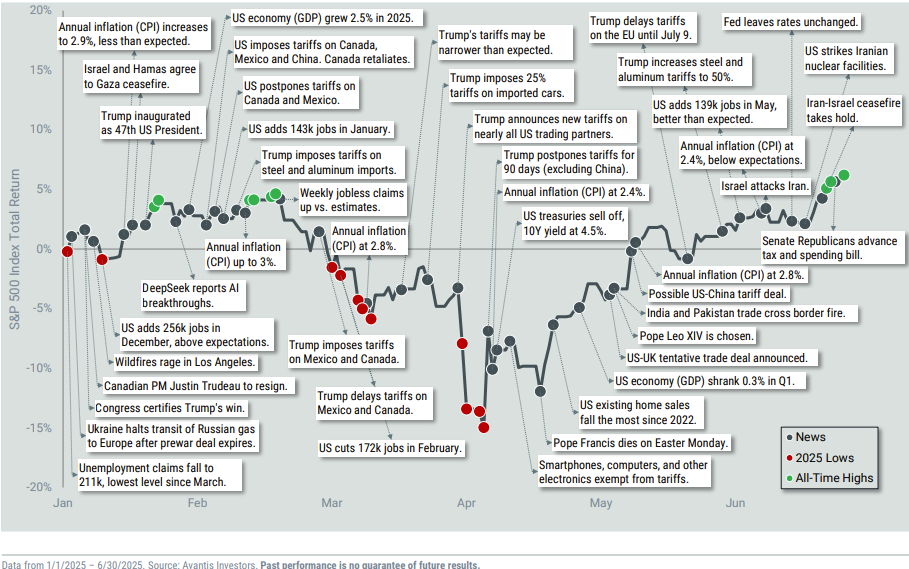

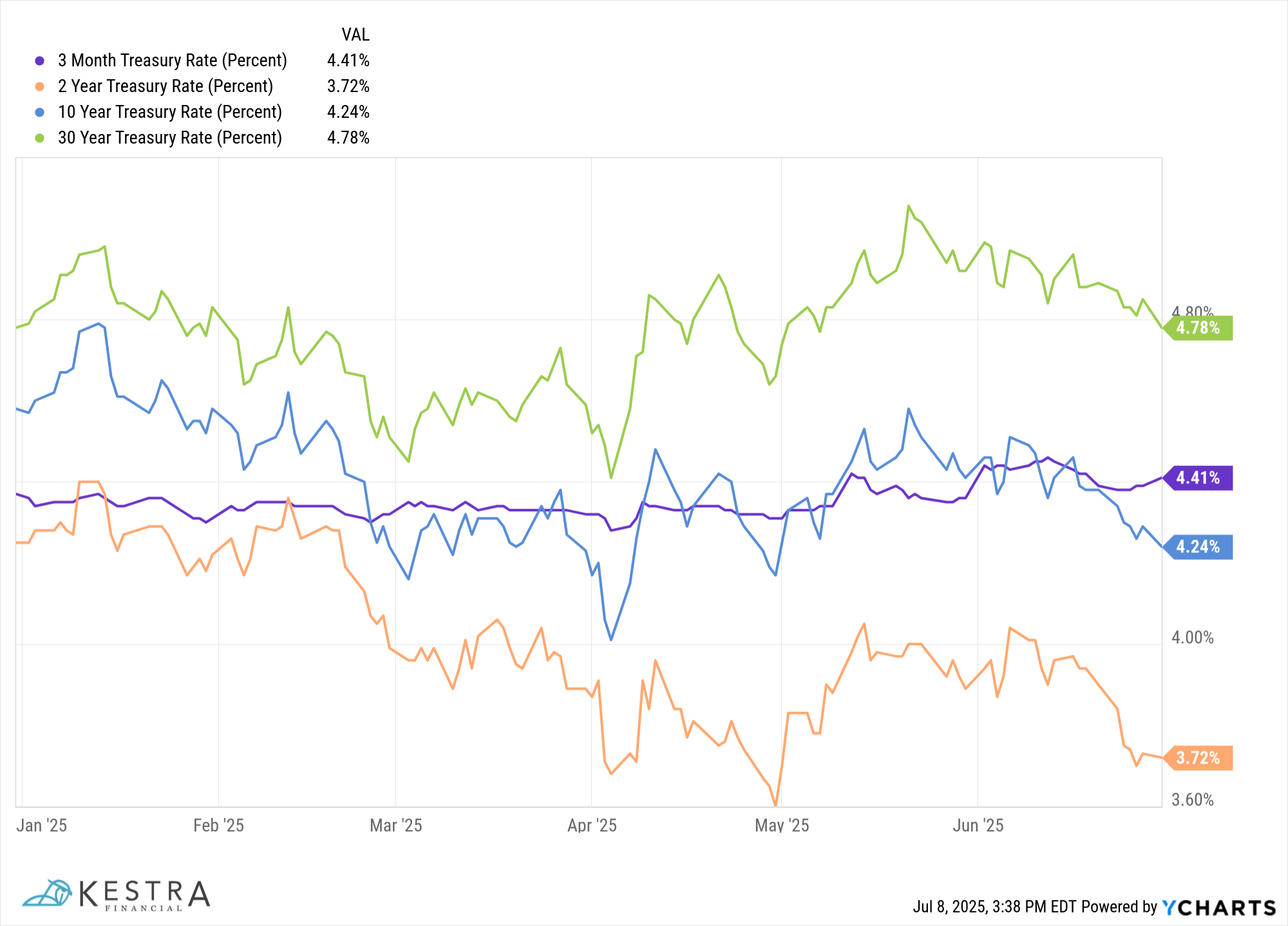

After an initial period of extremely volatile performance, markets rose in Q2, driven mostly by resilient economic data and moderate inflation. US equities posted gains as the labor market remained strong and consumer spending held up, despite concerns about higher interest rates. The Fed signaled it may hold rates steady for longer, pushing yields on longer-term bonds higher while shorter-term yields remained elevated. Overall, markets are continuing to digest a “higher for longer” interest rate environment

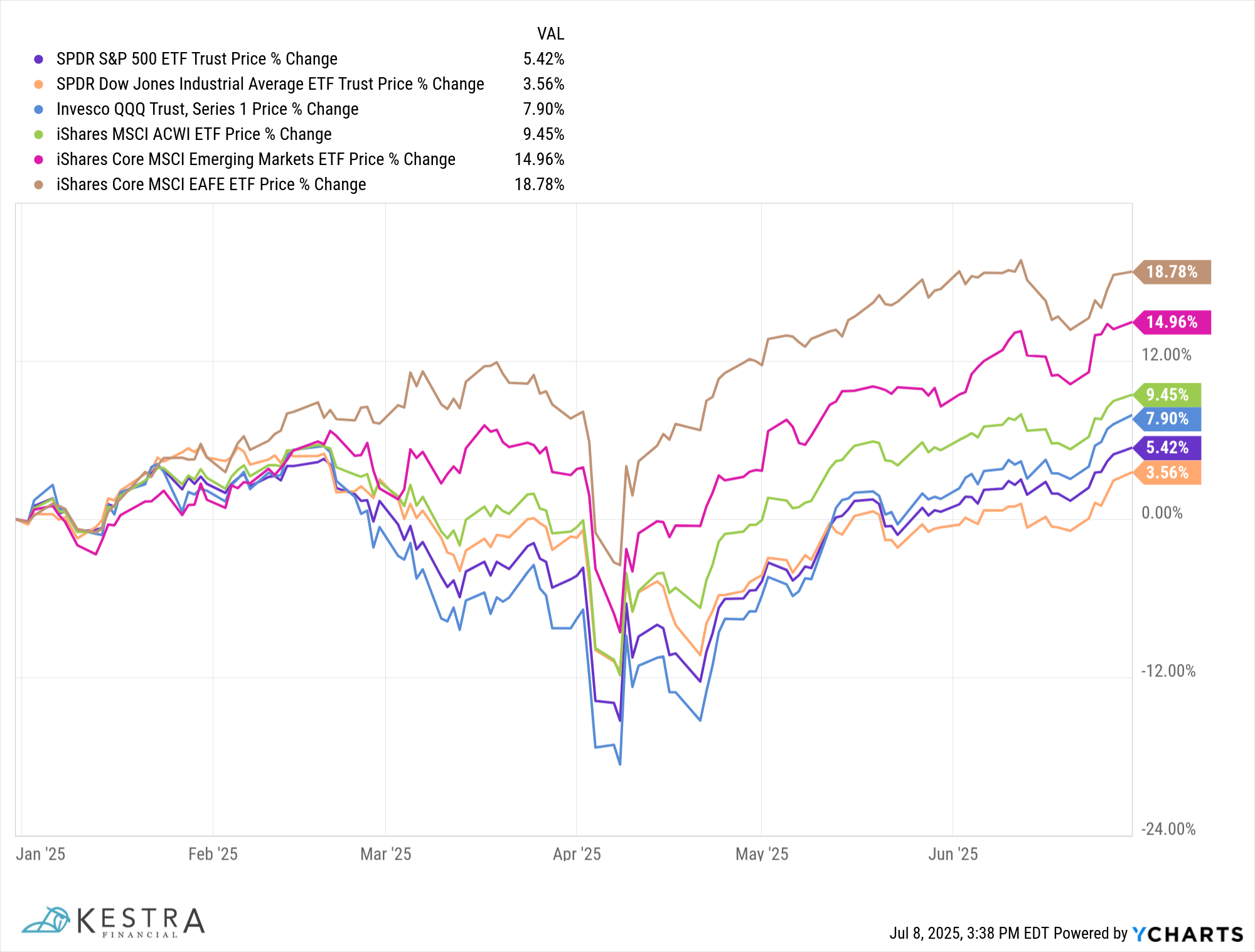

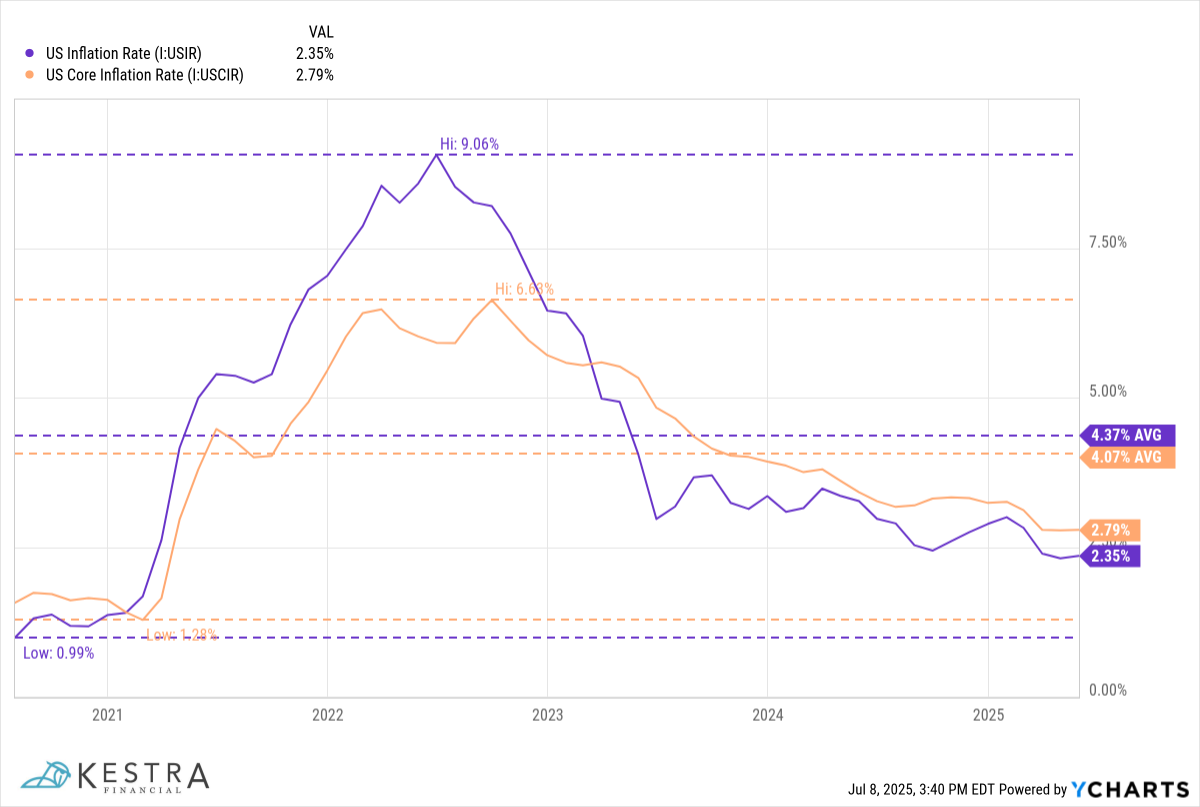

International stocks outperformed US stocks, though Europe faced weaker growth and China’s recovery has remained uneven. The quarter was marked by significant geopolitical events, including an escalation and eventual ceasefire in the Israel-Iran conflict, which drove bouts of volatility in global markets. Also adding to global market volatility was concern over global trade, with the US administration’s tariff decisions and the expiration of a major 90-day tariff reprieve in July. Inflation continued to cool, but remains above central bank targets, adding to the uncertainty around the timing of potential rate cuts.

Quarterly Spotlight Topic: Should I wait for rates to fall before investing in bonds?

With interest rates at their highest levels in years, many investors are wondering whether they should wait for rates to drop before investing in bonds, especially as equity markets continued to rally. This is a fair question, and one that we are hearing often from our clients – history shows us that trying to perfectly time the bond market, like the stock market, can lead to missed opportunities.

Bonds are mathematical instruments – when interest rates fall, prices rise, and vice versa. The timing and speed of these moves, however, are hard to predict. Today’s higher yields mean you’re getting paid more to be invested in fixed income instruments than you have been for the past decade – by staying on the sidelines, you risk missing out on current income and the potential price appreciation that can occur should rates decline.

It is also important to remember why bonds are in your portfolio as part of an overall investment strategy – bonds provide stability, diversification, and income to help balance the ups and downs of equities. Regardless of when you invest, today’s higher yields will help strengthen your plan over the long run. But rather than wait for the seemingly “perfect” moment to move funds into bonds, we believe in taking a long-term view, aligning your bond exposure to your goals, risk tolerance, and income needs.

If you’re wondering how bonds fit into your strategy in this rate environment or with additional uncertainty with the Fed and Federal Government, let’s discuss how to take advantage of current opportunities while keeping your bigger picture in mind.

All of the First Half of 2025 That Fits on One Page.

All of the First Half of 2025 That Fits on One Page.

International developed markets led global market performance, followed by emerging markets, the S&P, then the Dow.

International developed markets led global market performance, followed by emerging markets, the S&P, then the Dow.

Short-term interest rates remain relatively unchanged YTD, while longer-term rates have seen additional volatility with the uncertainty around Fed policy.

Short-term interest rates remain relatively unchanged YTD, while longer-term rates have seen additional volatility with the uncertainty around Fed policy.

Inflation rates remain slightly higher than the Fed’s target of 2% but are substantially lower than 2022 highs.

Inflation rates remain slightly higher than the Fed’s target of 2% but are substantially lower than 2022 highs.

The material is for informational purposes only. It represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. It is not guaranteed by any entity for accuracy, does not purport to be complete and is not intended to be used as a primary basis for investment decisions. It should also not be construed as advice meeting the particular investment needs of any investor.